- Report: #643759

Complaint Review: CitiFinancial Auto - Fort Worth Texas

Reported By:

stvnc10 -

San jose, California, United States of America

Submitted:

Updated:

-

Author Not Confirmed

Why?

CitiFinancial Auto

PO Box 961245 Fort Worth, 76161 Texas, United States of America

Phone:

888.222.4227

Web:

Categories:

Business Rating:

(0)

Tell us has your experience with this business or person been good?

CitiFinancial Auto Santander Consumer USA Inc Fraudulent Practices: Debt Collector saying that I owe money on a loan that has been paid. Fort Worth, Texas

Beware of Santander Consumer USA Inc., because they are crooks and liars.

I used to have an auto loan with CitiFinancial Auto, but I fell behind on my payments in 2009, so the collateral, or auto for which the loan was given was repossessed at the order of CitiFinancial Auto on September 30, 2009. That was twenty days after the last payment I had just made was credited to my account.

At the time of the repossession I owed $7,549.81. After CitiFinancial Auto received their collateral I was given a credit of approximately $5,549.81 on the loan and the account was closed one month later as paid. This was all done on their web site. Since that time I have received no correspondence from CitiFinancial Auto.

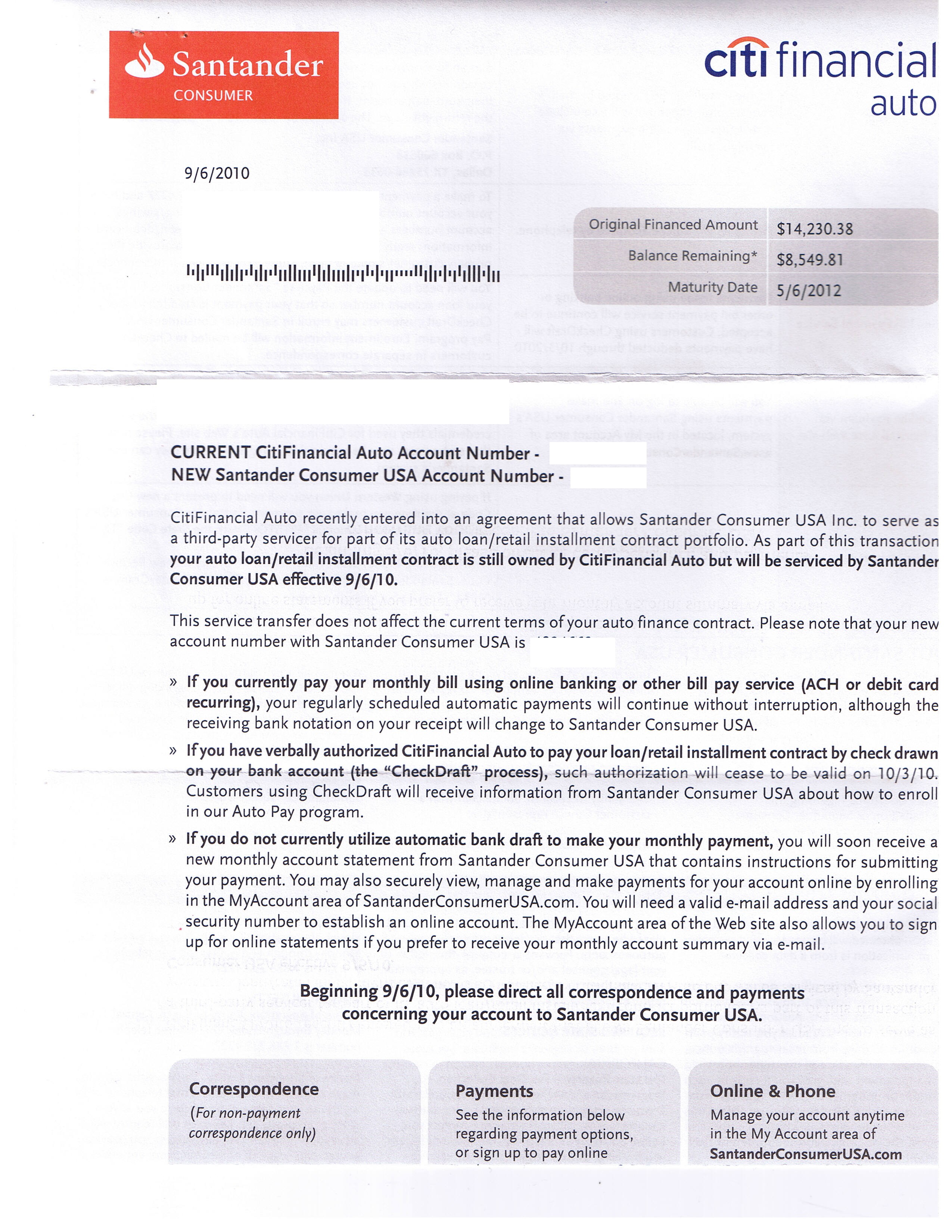

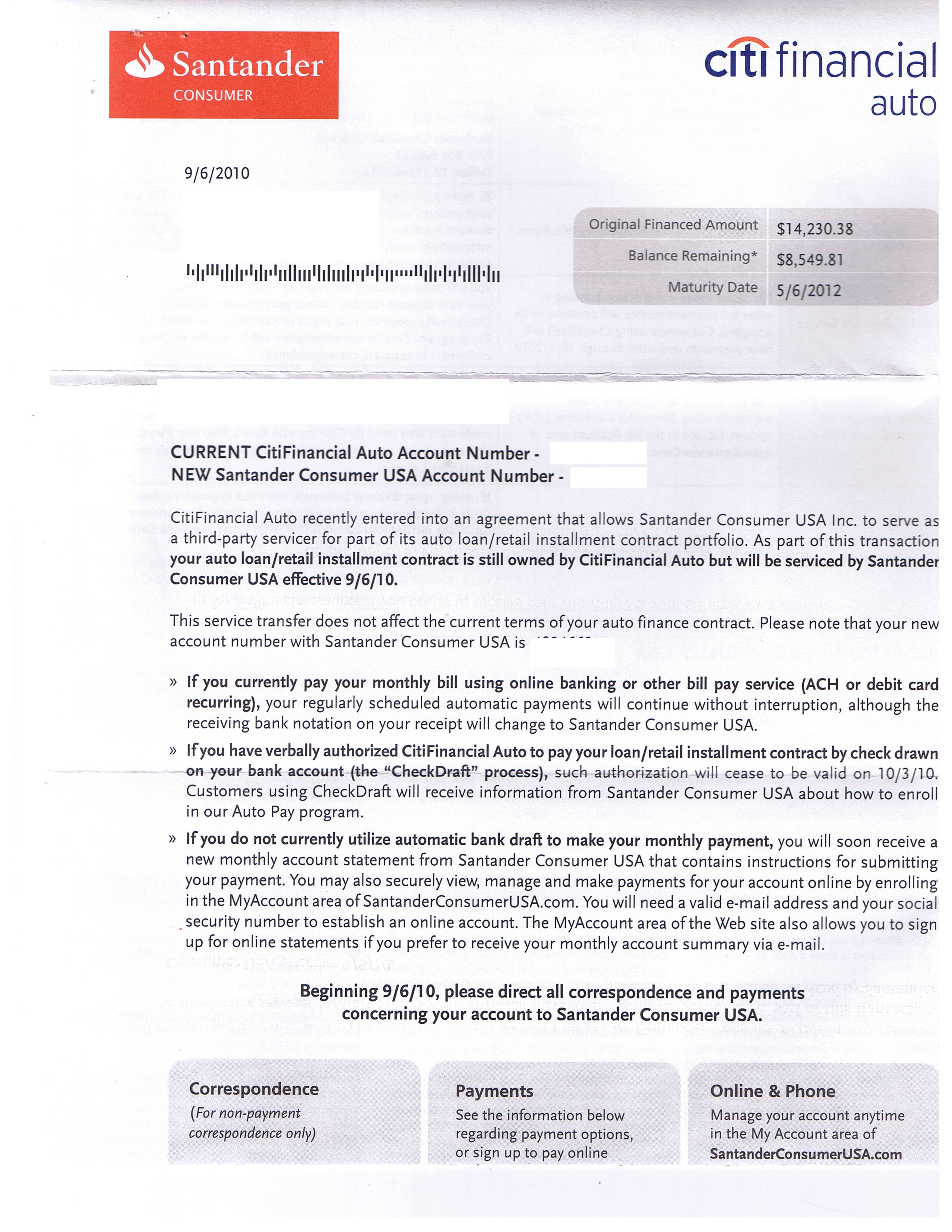

Almost a year later I received a statement with Letterhead "CitiFinancial Auto" and "Santander Consumer", on 09/22/2010, stating that I still owed $8,549.81 on this loan that I formerly had with CitiFinancial Auto, and that Santander Consumer USA Inc had been authorized to act as agents for CitiFinancial Auto to collect the debt.

I feel that this is a fraudulent attempt to collect a debt that I no longer have.

I used to have an auto loan with CitiFinancial Auto, but I fell behind on my payments in 2009, so the collateral, or auto for which the loan was given was repossessed at the order of CitiFinancial Auto on September 30, 2009. That was twenty days after the last payment I had just made was credited to my account.

At the time of the repossession I owed $7,549.81. After CitiFinancial Auto received their collateral I was given a credit of approximately $5,549.81 on the loan and the account was closed one month later as paid. This was all done on their web site. Since that time I have received no correspondence from CitiFinancial Auto.

Almost a year later I received a statement with Letterhead "CitiFinancial Auto" and "Santander Consumer", on 09/22/2010, stating that I still owed $8,549.81 on this loan that I formerly had with CitiFinancial Auto, and that Santander Consumer USA Inc had been authorized to act as agents for CitiFinancial Auto to collect the debt.

I feel that this is a fraudulent attempt to collect a debt that I no longer have.

5 Updates & Rebuttals

Tanya m

Erie,Pennsylvania,

U.S.A.

There are other fees involved other than interest.

#2General Comment

Thu, November 18, 2010

My sister had a car repossessed and the bank charged not only what the balance was after they sold the car but also the repossession fees and other court costs. Ask your bank the break down of what you owe and why you owe it. They are required to give you a copy of it. Just thought I'd throw that in.

stvnc10

San jose,California,

United States of America

So what?

#3Author of original report

Sat, September 25, 2010

It is true that I committed breach of contract first, because I fell behind on my payments, but two breaches or two wrongs don't make a right, nor does one party breaching a contract give the other party the same right.

The letter that I received was a communication from a debt collector because it said so on the back.

Thank you for pointing out the obvious, that I need paperwork to prove my point. I always save my paperwork, sometimes for up to ten years.

Anyway, I really don't care about the outcome very much, I just wanted to report that CityFinancial Auto and Santander are not the good guys here. They use unethical business practices by telling me that I owed them more than I do. I don't care about any possible reasons for the action, I just care about the action It is Fraud.

Fraud is saying something that isn't true, telling someone that they owe more than they do is saying something that isn't true. Before telling someone that they owe X amount of $ they need to be certain of the amount.

I've noticed after reading many of the articles about CityFinancial Auto and Santander that most of the Rebuttals are trying to discredit the authors of the posts. To the people submitting these Rebuttals, we know who you work for and what you are about.

To Flynrider and Robert, thank you very much for your comments and advice. I found them very well thought out and constructive.

Robert

Irvine,California,

U.S.A.

Well..

#4Consumer Comment

Fri, September 24, 2010

Before you start to go off screaming "breach of contract" you probably should remember that YOU fell behind on the payments and had the car reposessed. By the way if they come and get it or you turned it in, it is still a reposession.

If you have some other insurance that covers reposession you better drop everything and start looking through all of your paperwork to find it. However, The only "insurance" I can think of that you may be thinking of is GAP insurance. That does protect them if your car gets stolen, totalled, or other loss. But it DOES NOT cover you missing the payments and having the car reposessed.

The item I do agree with you on is the amount. If your numbers are right, then over $6,500 in interest in a year does appear to be excessive. But without knowing your original terms, and if in fact the "numbers" you have are correct it is hard to say for sure. However, in looking at the letter it seems as if this may be something else.

It does not appear to be a "collection letter", it appears that Santander may have taken over your loan and for some reason still show it as open. Whether this is an "error" on their part or with Citi is something that you may have to look into. Because what would be more logical is that if your balance was $7,500 an extra $1000 in interest in a year is not that out of the ordinary especially if you didn't pay. The problem is that if you call Santander you may start up collection procedures on the amount you do owe. So you better have all of your paperwork in order before you start to investigate this. It is also very possible that you are correct and citi forgave that $2,000 and you don't owe anything. But without paperwork to show that it is going to be hard(if not impossible) to prove.

stvnc10

San jose,California,

United States of America

Who Knows? But good point.

#5Author of original report

Fri, September 24, 2010

I don't know about owing the $2000, maybe I do. But I did have some kind of insurance on the loan protecting them from my default. I don't know all of the details of how the insurance worked, but I think that it covered the remaining $2000 so the insurance paid the balance owed. However, if I did owe them $2000 then it seems logical to me that I would have heard from them about it over the last year. You know, like a letter telling me so, demanding payment and offering to set up a payment schedule. In my experience that is what usually happens because, as you say, they want their money back. But I haven't received anything from them until this notice from Santander almost a year later stating that my account balance is $8549.81. If I did owe them the $2000 as you say I might what is $8549.81 minus $2000, I think it is $6549.81 isn't it? That is quite a large inflation, over three times what you think that I owe, without any previous explanation. How and where is that legal?

Have a case for collection? I really do hope that they pursue the matter in court. Ever hear of breach of contract? If they change the terms of the loan contract they have to give me notice of the change at least 30 days before it happens. They did not do this.

My point is; they are trying to collect an amount of money from me that I do not owe them. They are telling me that I owe them X$ when I do not. That is fraudulent, because they are trying to fool me into thinking that I owe them money that I do not owe them.

Report Attachments

Flynrider

Phoenix,Arizona,

USA

I see a problem.

#6Consumer Comment

Fri, September 24, 2010

If you still owed $7549 and the collateral turned out to be worth $5549, why do you think the debt was satisfied? According to my math, you were about $2,000 short. I have no doubt that they closed the account after the repo, but what makes you think they magnanimously forgave the $2K. That never happens in the real world.

No doubt the collectors have inflated the original number. They usually do. But unless you have some piece of paper that shows CitiFinancial forgiving the balance on the debt, they probably have a case for collection.