- Report: #652512

Complaint Review: Chevron - Orlando Florida

Reported By:

andromedagirl -

Orlando, Florida, United States of America

Submitted:

Updated:

-

Author Not Confirmed

Why?

Chevron

1601 E. Colonial Orlando, 32803 Florida, United States of America

Phone:

407-896-1382

Web:

Categories:

Business Rating:

(0)

Tell us has your experience with this business or person been good?

Chevron puts $90 hold on bank account for $23 gas purchase -- WTF????!!! Orlando, Florida

*Consumer Comment: It's the banks doing this..

*Consumer Comment: I have to disagree with you Ronnie...

*Consumer Comment: It varies.

*Consumer Comment: I overlooked...

*Consumer Comment: You'll get the money back...

*Consumer Suggestion: Use your PIN# and it will process right away

*Consumer Comment: Vote with your dollars...watch out for your own wallet.

*Consumer Comment: Not exactly how it works.

*Consumer Comment: Point taken

*Consumer Comment: Wrong about the bank

*Consumer Comment: Uh..this report is like 2 years old???

*Consumer Comment: it isnt the banks

*Consumer Comment: Gas stations blame banks for a reason....

*Consumer Comment: Thing is Buddy...

*General Comment: Few minutes?

*General Comment: now higher yet

*Consumer Comment: Chevron still at it....

*REBUTTAL Owner of company: Use your pin on debit card for gas purchase

So I went to this Chevron gas station near downtown Orlando to purchase $23 of gas. I charged it with my Visa debit card, which is tied to my checking account at Suntrust bank.

Got home and logged onto the Suntrust website to check my bank balance, only to find that the Chevron gas station charged me not $23--- but $90!!!!

I immediately called Suntrust to report it as a fraudulent charge, but the customer service rep said they have taken countless phone calls on this very issue today. The rep said this is something that Chevron and Texaco are doing now. They are letting customers swipe their debit cards at the pumps to pay for gas, and in return they are putting $90 holds on their bank accounts for 3-5 business days.

She said it will take 3-5 days for it to cycle out, and that eventually the correct $23 charge will be registered to my account.

But in the meantime, my money has been hijacked by Chevron and I'm screwed. So, warning! What's worse is that the gas station didn't even have any signs posted warning customers that this will happen. That's a sweet deal for the gas station, I guess!

18 Updates & Rebuttals

Dorothy Cannon

whitesettlement,Texas,

Use your pin on debit card for gas purchase

#2REBUTTAL Owner of company

Thu, December 18, 2014

Hay I can tell you as a gas consumer using your pin on debit card does not help .I used my debit card to get gas on outside at 7/11 here in Whitesettlement Texas and put in my pin number and it it still took out a hundred dollars for a 5 dollar gas purchase .No signs anywhere warning you and I didnt know they did it till after I got home and my ace card sent me an email stating I had a 95 dollar purchase when all I got was 5 bucks on gas .I do have the gas reciept showing 5 dollar purchase with my debit card number on it .I am looking into sueing someone cause someone has my money for what will be 7 days and that money is making someone money interest ect .If banks are using it they make way more interest off money then the public does .And if the pump can tell you you dont have enough money to buy gas then they know if you have funds or not same as anyone else .You dont see other merchants putting holds on your money .This is illegal period no matter who's the blame you did not authorise it .I sure did not and there was no sign warning you either .Maybe we need to go though commercial contract courtroom to get something done .I know its wrong and they can be sued over it .Also 7/11 bought out chevron gas here in Texas .I also now know this is what happened on my vacation to Galvaston a few years back .I think one of the guys above is right if credit and bank companies cant straiten it out maybe using cash is the better deal for consumers exspecialy for hotels .So folks dont think if you use debit and punch in your pin number it will not put a hold on your money they do just had it happen to me last night and it close to christmas .

Kat

Pensacola,Florida,

Chevron still at it....

#3Consumer Comment

Sun, March 30, 2014

My husband just filled up his Harley along I-10 in Florida and Chevron put a $126 hold on our debit card. This is ridiculous. The explanantion that it's to avoid drive-offs is also ridiculous. Once you swipe your card the station has your info. And the pump won't even come on till the card is accepted. So how exactly does it deter people from driving off without paying? In this day and age of technology, there is no reason a Chevron customer should be out $126 for 3 or more days while the charge awaits approval. And when someone's account goes in the hole becasue of the outrageous hold, they are subject to overdraft fees if they still have other items that need to clear their account. Bad bad practice by Chevron.

kstm

Georgia,United States of America

now higher yet

#4General Comment

Tue, September 04, 2012

as of now, chevron is preauthorize 126.00 to your card, then the charge of the gas on top of that, then it takes a day or two for the 126.00 pre authorization too come off your card, can yu imagine the amount of money they are making on interest alone for that day? and if you are one that has a small CC you are probably going to get a over limit fee from your cc company!

bottom line, do not use chevron any more!

Flynrider

Phoenix,Arizona,

USA

Few minutes?

#5General Comment

Wed, August 29, 2012

" Either way that hold should only be for a few minutes if that. To hold that much for days without the authorization (or even knowledge) of the customer should be unlawful and can certainly cause financial problems and overdrafts. "

You are obviously having trouble understanding how this works. The hold is placed by the retailer (not the bank) to ensure that funds will be in the account when the actual transaction posts to the customer's account. The process of posting a transaction to a customer's account can take 3 - 5 days, depending on the retailer, their card processor and the other middlemen. There would be no point for a hold that lasts only a few minutes if the account was empty by the time the transaction actually posted.

Your fervent belief in gas station stickers should be tempered by a little logic. You can figure this out by using that time honored cliche from the Watergate era : Follow the money.

The retailer is the only one that benefits from the hold. It ensures that they will not find out in 3 - 5 days that their transaction was rejected due to a lack of funds in the customers account. When that happens, they take the loss. The bank has no interest (literally and figuratively) in placing a hold (they get their money for free from the Fed). The fact that the hold amount varies widely from retailer to retailer should also be an obvious tipoff as to who is really placing the hold. Why would my bank have 4 different hold amounts from 4 different gas retailers on the same card. The obvious answer is that the retailer determines the hold (Stickers not withstanding).

Ronny g

North hollywood,California,

USA

Thing is Buddy...

#6Consumer Comment

Fri, August 17, 2012

When you slide a card at the pump and it does not matter if it is credit or debit..the pump does not know how much you are going to pump...and neither does the merchant or the bank.

The merchant and the bank also do not know how big of a tank you have...some people have large trucks with two huge tanks...the pump does not know this. Gas is going up so yes, the holds will be more then they used to.

Now for example if you only have 20 dollars in the account, without a certain hold you could certainly pump more then 20. The pump DOES know how much is in your account has if there is not enough to cover the hold, the transaction is declined and you are requested to see the attendant inside. This way as long as your card had at least 20 bucks on it, you can tell the attendant you want 20 bucks of gas and it will work fine.

What gets me is why some people are having this hold for so long. Sometimes they just hold a dollar which is really just to make sure the card is legit...some hold a larger amount which is to make sure there is enough in the account to cover someone who is going to fill up with a lot of gas. Either way that hold should only be for a few minutes if that. To hold that much for days without the authorization (or even knowledge) of the customer should be unlawful and can certainly cause financial problems and overdrafts. This is why it is important to know who is doing this. Since the pumps I have used have this decal stating it is the customers bank doing this and really would do the merchant no good to hold the money I have to still say it is YOUR bank doing this for whatever reason and you might want to talk to them about it. If the bank has nothing to do with this then the merchant could be sued for posting that decal which would be outright fraud. So look into it. You won't always get the truth here but someone knows for sure.

MovingForward

Palm Beach Gardens,Florida,

USA

Gas stations blame banks for a reason....

#7Consumer Comment

Thu, August 16, 2012

I read that sticker you posted. It does sound like the gas station is putting the "blame" on the bank for withholding funds out of the account. If I had to guess, and that's all I'm doing, I would say the gas station doesn't want to face the flack from the holds so they place the blame elsewhere. It doesn't make logical sense for the amount to vary from gas station to gas station if it were the bank withholding the funds, does it? It would be a consistent amount from one gas station to the next if your bank had the authority to institute the hold. But the amounts held vary from $1 to $100 and in some cases more in the vary same region with the same vendor. The only difference is the actual station you use to fill up your tank. That's why I believe the posters above when they say it comes from the station owner.

buddy

pelham,Alabama,

United States of America

it isnt the banks

#8Consumer Comment

Thu, August 16, 2012

it isnt the banks doing it. it is chevron and that is where the charge is coming from. an ATM isnt going to give you $300 when you have $10 in the bank.why cant the gas pump check the balance like an ATM does. to hold $125.00 for 3 days on a $20.00 gas charge is criminal.cars cant even hold $125.00 of gas what chevron charged me this morning.i have never seen a charge like that in my life and i use my card all the time.

Ronny g

North hollywood,California,

USA

Uh..this report is like 2 years old???

#9Consumer Comment

Wed, April 04, 2012

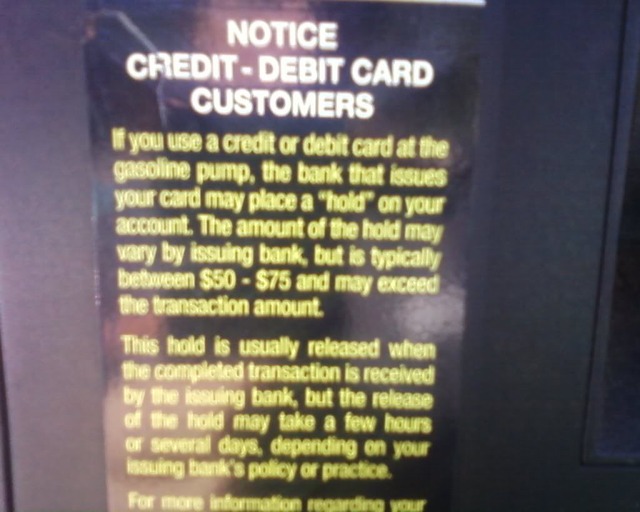

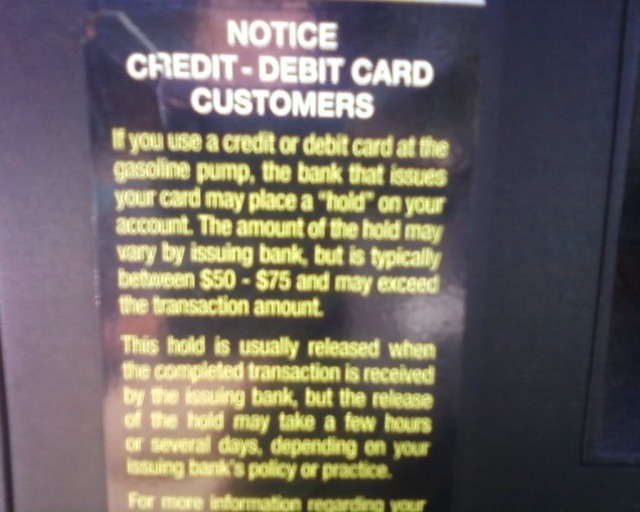

My reply in this case posting the info of that it is the BANKS determining the hold amounts and length of time is based ONLY on the decal I discovered on the gas pumps in my local...which I will post the pic of AGAIN in response on the bottom of this reply.

So...look at the pic and tell me what else you can logically conclude and we will debate from there...

Report Attachments

Amanda B

United States of AmericaWrong about the bank

#10Consumer Comment

Wed, April 04, 2012

Sorry, Ronnie, but this is incorrect information. It is in fact the gas station doing the holding/hijacking of money. I spoke with the gas station just a few moments ago, and they said this is their "new policy".

My credit union doesn't do any holding of money. I have been with them for years, and they have never done this. I also called them, and they said they don't even have the power to do this, only the store reports the money needed, and that's what's held.

The amount held (in my case, $126) is sent through as a hold before the final number of actual cost (in my case, $66) is ever even obtained. The bank wouldn't even know what to hold so early in the game.

MovingForward

Wellington,Florida,

United States of America

Point taken

#11Consumer Comment

Thu, October 21, 2010

Ok, you are on point about the extra funds not going to Chevron. As you pointed out, the additional funds over your actual purchase are temporarily removed from usage in your bank account in the case of a debit card or from your limit with a credit card. In any event, our funds are not available to us to use for 3 to 5 days.

My main point is this: as consumers we have the ultimate choice of which gas station we choose to use. Don't use the stations that place a hold on additional funds over the cost of the service.

There are stations that just charge you for the exact amount of gas you pumped at the time you pumped the fuel. Why would you use a station that places an extra amount on hold? If enough people are aware of the practice and stop patronizing the offending gas stations, then management will adjust their policy or go out of business.

Flynrider

Phoenix,Arizona,

USA

Not exactly how it works.

#12Consumer Comment

Thu, October 21, 2010

"Why should Chevron get an extra $75 (or $90 in the author's example) to use for 3 to 5 days? If you fill up twice a week then Chevron has had your money for a minimum of 6 days. It's great cash flow for Chevron - terrible money management for you or me. "

Chevron does not get the $75 to use for 3 to 5 days. They don't get anything at all by placing the hold. The only purpose for the hold is to verify at the point of purchase that you have at least x dollars. The hold goes to your bank and x dollars are reserved from either your balance (if it was a debit card) or your credit limit (if it was a credit card). At no time does the retailer actually get the amount of the reserve. The hold will either expire in 3-5 days, or it will disappear when the actual purchase amount of the transaction is posted to your account.

MovingForward

Wellington,Florida,

United States of America

Vote with your dollars...watch out for your own wallet.

#13Consumer Comment

Thu, October 21, 2010

So it seems to be an individual station owner's choice rather than the entire company that selects the amount of your money to hold while simultaneously charging you the amount you actually spent.

In that case the solution is easy: don't buy gas from those gas stations with the extra hold in place (no matter the amount). Why should Chevron get an extra $75 (or $90 in the author's example) to use for 3 to 5 days? If you fill up twice a week then Chevron has had your money for a minimum of 6 days. It's great cash flow for Chevron - terrible money management for you or me.

There are plenty of stations that just charge you the amount you actually pumped. Reward the gas station that does not charge you extra by buying your gas there. You know which gas stations don't have the extra charge in your local area. (Maybe someone will come up with a phone app that shows which stations don't have that extra charge. :))

If enough people don't purchase gas at the station due to the station owner's policy of taking extra funds, then the station owner will eventually notice. He/she can then change his policy - or lose his business. Vote with your wallet...don't give Chevron (or Shell or Texaco) your 'extra money'.

Steve

Bradenton,Florida,

U.S.A.

Use your PIN# and it will process right away

#14Consumer Suggestion

Thu, October 21, 2010

I have encountered this myself with my debit card, BUT that is only when you just jam yhe card into the pump and use it as "credit".

If you selct "debit" and input your pin, the tranaction processes immediately, no excess hold amount. It processes for the exact amount and you see it by the next morning at the latest.

Edgeman

Chico,California,

U.S.A.

You'll get the money back...

#15Consumer Comment

Thu, October 21, 2010

This is a hold put in place by the gas station, not the bank. $90 does seem a bit high but not every Chevron does this. My local Chevrons used to place a hold of just $1 against my account but recently they switched to placing a hold for the exact purchase amount. Because of this, I suspect that the $90 was set by the owner or management of that particular station.

If you want to avoid a hold, try going inside and prepaying for a certain amount of gasoline. That way you know how much will be held and you can always go back for the change if you don't use all of it for gas.

Ronny g

North hollywood,California,

USA

I overlooked...

#16Consumer Comment

Thu, October 21, 2010

..the fact that the hold amounts may vary from state to state.

But either way..this decision as far as I am aware..is the BANKS..and not the merchants.

Perhaps this requires further investigation? The only facts I have to go by..is what I read as public documentation regarding the regulations....and what it says on the sticker affixed to the gas pump...and the sticker affixed to the gas pump CLEARLY implies..no, not implies..but STATES.. that this hold amount...and length of time of said hold..is decided by on YOUR bank.

Perhaps it is time you go back to the pump..break out your magnifying glass..and report back what the affixed sticker/decal says regarding the hold. Oh trust me..it is there, but as I previously stated..it is small.

Put it this way..I had to look for it with INTENT, in order to notice it.

Flynrider

Phoenix,Arizona,

USA

It varies.

#17Consumer Comment

Thu, October 21, 2010

Both in location and company. You cannot depend on getting a $1 hold just because you choose credit (although it's common in my local area). The retailer decides what kind of hold will be placed. For example, In my local area, the Texaco and Chevron company owned stations all use a $1 hold for credit cards. The quickie mart down the road, which sells Chevron gas, uses a $50 hold. I swiped my card at a city owned Phillips aviation gas pump the other day and ended up with a $200 hold.

If you must use a card, the safest bet is to use a credit card that is not anywhere near its limit. That way, the hold does not tie up your actual money (like a debit card does). It just ties up some virtual dollars on your credit limit.

MovingForward

Wellington,Florida,

United States of America

I have to disagree with you Ronnie...

#18Consumer Comment

Wed, October 20, 2010

You said just "choose credit" and they won't hold the $90. I have not found that to be the case here in S Fl. When I use my debit card as a credit card at the pump it will hold not only the amount I pumped, say $50 - it will ALSO hold out a specified amount, $75 seems to be common. The additional $75 is taken for 3 days.

The OP had $90 taken out of the account. My suggestion is to avoid both Chevron and Texaco. Shop elsewhere with your gas dollars - that's what I am doing. I had two vendors (Shell and Chevron) on my list of places not to buy gas. I just added Texaco because of this post. Thanks for the heads up.

Ronny g

North hollywood,California,

USA

It's the banks doing this..

#19Consumer Comment

Wed, October 20, 2010

..and for good reason.

You see the recent regulation changes have made it so the banks can no longer automatically enroll you in standard overdraft protection with the debit card...nor can they force you to enroll.

There is a flaw in the system which is being looked into..but this flaw is allowing some to "fall through the cracks" so to speak.

You see...if the bank can not allow a transaction to be approved if the account can not cover it..how do they protect themselves in the event someone swipes a debit card that has 20 dollars in the account...but decides to pump in 40 dollars in gas?

The only way they can do this is by placing a hold. This should be on a sticker affixed to the gas pump..albeit it is small. At least here in my local gas stations it states the hold will be from 50-75 dollars...and can last up to 3 days. Usually this hold is gone before I even notice it..but one time it did take until 5AM...I was a bit concerned but by the time I got up in the morning for work, the hold was gone. I have had holds from restaurants however stay on there a week. This did require action on my part which was to walk back into the restaurant and tell them I am lodging a dispute for an unauthorized charge...seems to do the trick.

Here is the best way to avoid this. One is..to choose "credit"...but the problem with that is it can still overdraft the account (even though it only runs one dollar threw to check if the account is valid), and this can subject you to an overdraft fee if you pump in more then you have to cover it in the account. And the fee is not a "hold"..the bank will charge you that if you overdraft and not much you can do.

The second option is to pay inside..tell the attendant what you wish to pump in..and if the account can cover it, all is well.

The third option which is the BEST bet..as always..CASH. CASH is still king.