- Report: #1485591

Complaint Review: Paparazzi Motors LLC - Fort Myers Florida

Reported By:

Making Others Aware -

Sebring , Florida, United States

Submitted:

Updated:

-

Author Not Confirmed

Why?

Paparazzi Motors LLC

1295 Tamiami Trail Fort Myers, 33903 Florida, United States

Phone:

239-349-7905

Web:

Paparazzimotors.com

Categories:

Business Rating:

(0)

Tell us has your experience with this business or person been good?

Paparazzi Motors LLC Paparazzi Motors Repo-ed a vehicle when payments were made Fort Myers Florida

Report Attachments

Our payment for September was due on the 5th. We stayed in communication with Paparazzi Motors, LLC and notified them via Facebook (as we always do) that our payment would be late and we would make a payment on September 13,2019.

On September 14th, I attempted to make a payment after letting Valerie know that I was at the bank getting a new debit card. I contacted the office & attempted to take a payment & it would not process. I then attempted to make an online payment & it was not accepted. We let the office know via Facebook messenger.

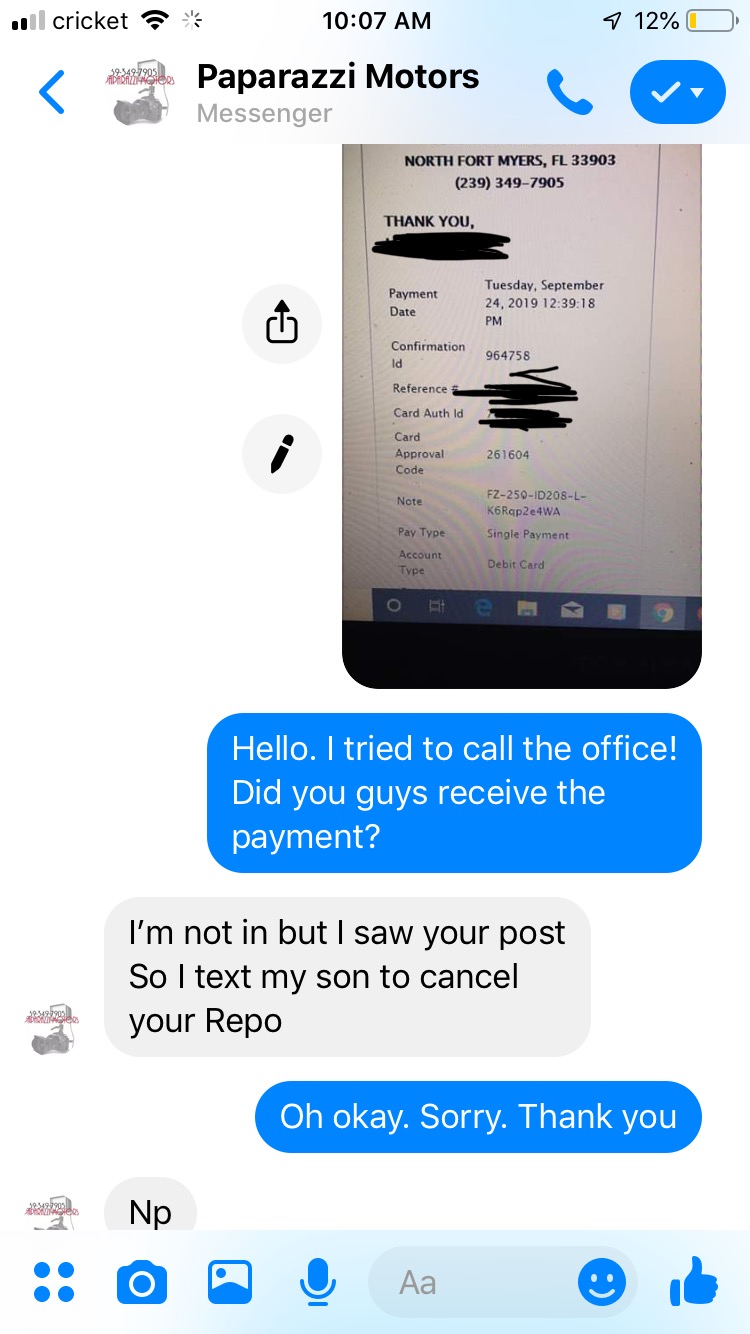

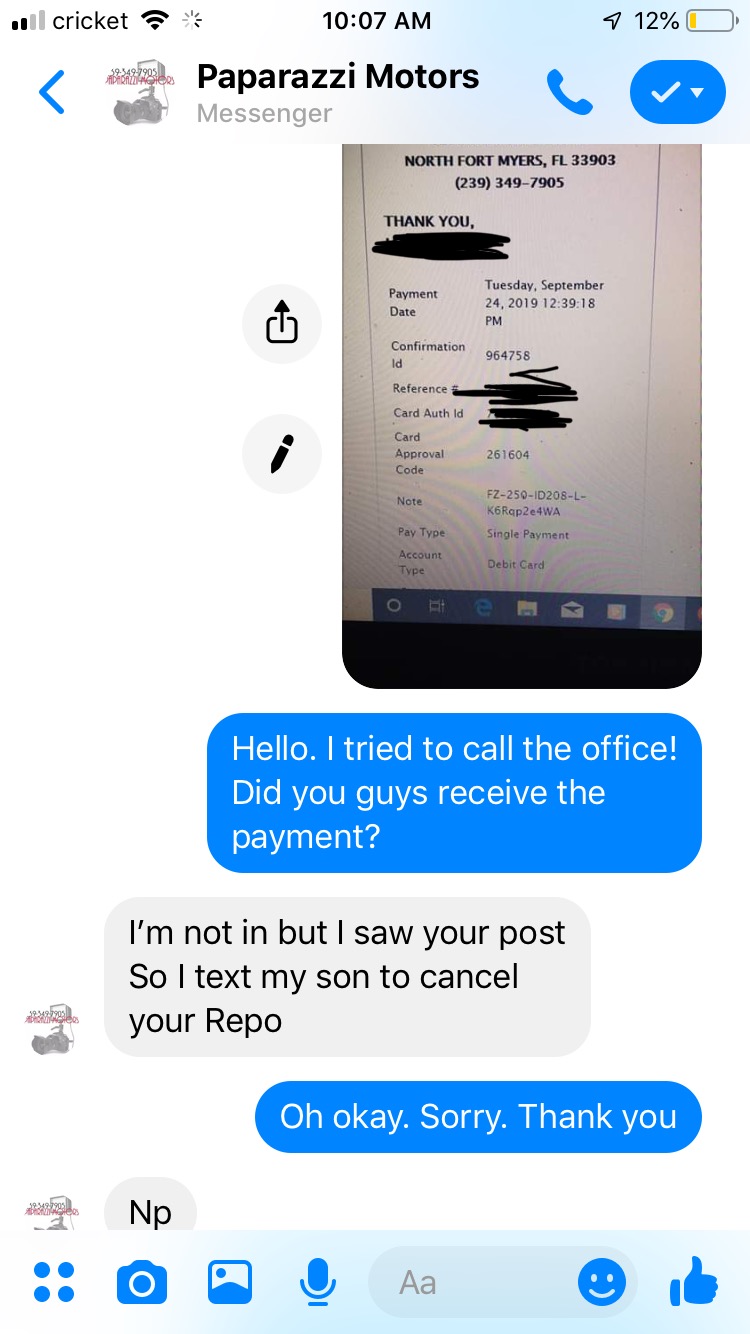

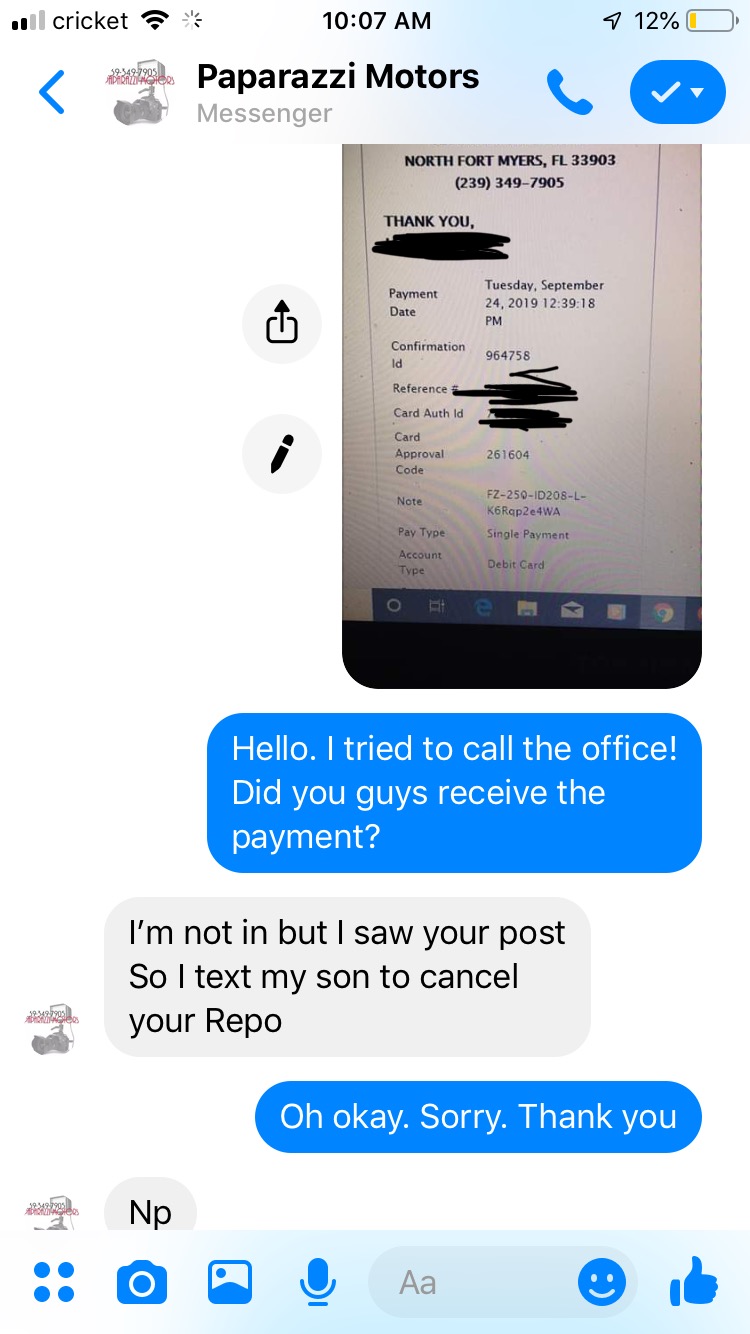

On 09/17/19 we had a family death, we let Valerie know the issue & that we would do our best to make time to bring the payment since the online was not working. Valerie said that was fine. On September 24, 2019, my sister made an online payment for $319.12 & it was accepted.

I called the office to let them know since there was no answer, I messaged the business Facebook page to make them aware of the payment. Valerie stated that she was not at work but she would had texted her son to have him cancel the repo. We were unaware of the repo.

My husband saw a tow truck and waved him down. He stated that he had to take the vehicle. We let him know and showed proof of a payment being made and Valerie stating that she was having her son cancel the repo. The boss, John Lewis, of the tow truck driver said he needed the vehicle or he was contacting LEO.

We contacted Valerie who then stated that there would be a $500 repo fee (at this point the vehicle had not been touched by the repo guy or his truck) and if we could pay at least half of it and they will let us keep the car.

My husband and I both spoke to John who said he was from Dealer Lending (unsure if this is true) & he stated if we gave him possession of the vehicle he will do a condition report and then give us a lower interest rate and we can get the car back.

After giving them possession of the car with agreement we would get it back on Wednesday September 25, 2019 and them constantly threatening to call LEO and have everyone arrested, Valerie then reversed the payment and said that it was at the request of John whom was suppose to be the contract owner of our vehicle loan.

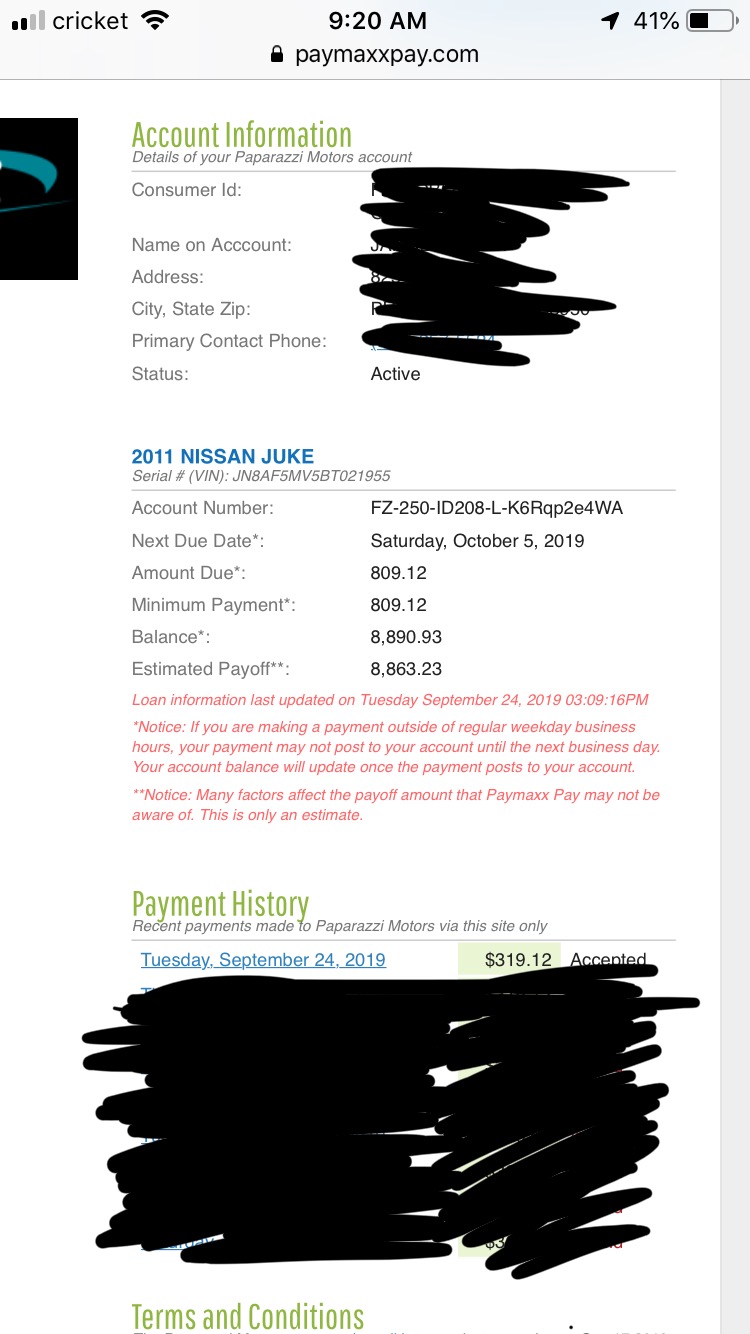

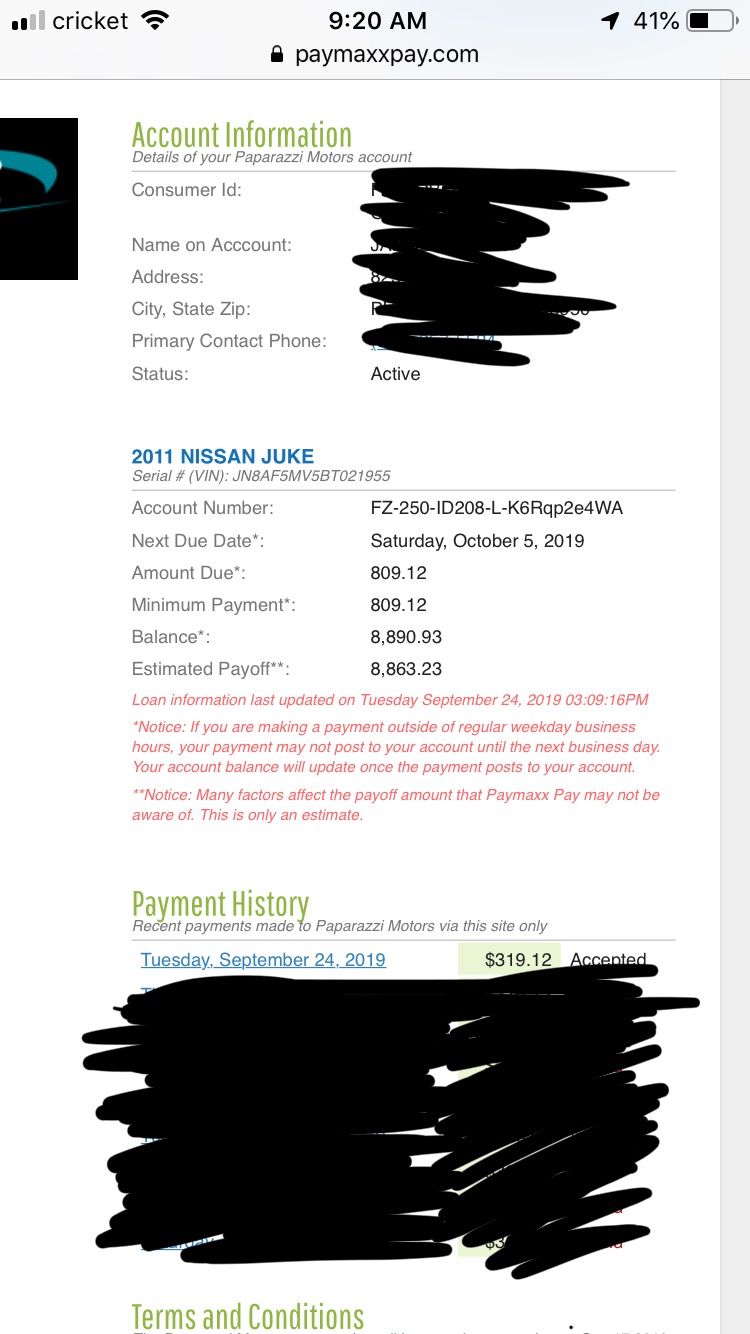

After Valerie reversed the payment we looked online and seen the payment amount had been updated to $809.12 which now includes the repo fee. However, payment of $319.12 had been made before the repo guy found the address and eventouched the vehicle.

4 Updates & Rebuttals

John

Takoma Park,United States

In the end....

#2General Comment

Fri, September 27, 2019

Your payment was THREE WEEKS LATE. No amount of Facebook posting, "notifying," or "attempts to make online payments" changes that. You broke your contract and lost THEIR car and all the excuses in the world doesn't change that simple fact.

By the time you made a payment the next payment was only days away- did you have the money to make that, or were you going to do more "notifying" and less paying in October, too?

John

Takoma Park,United States

Endless Excuses.

#3General Comment

Fri, September 27, 2019

Seriously, is this a joke?

You agreed to make payments on a certain date. Knowing you'd be late, you did the "responsible" thing and "notified" your creditor you'd make a payment on September 13 (via a Facebook post- not by calling, which is what a responsible person not trying to slyly duck responsibility would do. BTW, why did you think it was ok to be late as long as you let them know you'd be late? That's not how contracts work.)

So what happens on the 13th? Apparently nothing- next thing you tell us is that you called on the FOURTEENTH to tell the creditor that you were in the process of getting a "new debit card"- why is this information important to the creditor? They just want their money- the money you agreed to pay.

Days go by. Now something else has happened to "prevent" you from making the scheduled payment. You're online, you're making phone calls- you do everything but actually just go to the place of business and hand over cash, because that would actually cost you something. You keep saying you'll "do your best to make time to bring the payment since the online was not working," shifting the blame on to the company for not having a functioning website that could take online payments- but this is AFTER YOU WERE ALREADY LATE. And I'm pretty sure that your contract doesn't say "make payments on time unless the online payment option doesn't work and you can't make time."

Someone named "Valerie" tells you that a late payment is "just fine," and ELEVEN DAYS after the due date- TEN days after you SAID you'd pay- you finally make an ONLINE PAYMENT.

"Your" car gets repossessed by a company that apparently had an employee who misunderstood the company policy- this is not their problem. You broke the contract, you meandered all over the place and spent more time inventing excuses than actually making payments, and now you're all upset because your creditor took THEIR car back.

They had every right to repo THEIR car. If you want it back, you'll pay a Stupid Tax Repo Fee you could have avoided if you had just been an adult and recognized that your personal problems can't be used to cancel or alter contracts. Seriously. Sorry for all your problems but there was no ripoff here.

Robert

Irvine,California,

United States

Another Self-Entitled Deadbeat

#4Consumer Comment

Fri, September 27, 2019

Wow...just another classic post from someone who thinks that they can change contract terms and people just need to accept it.

notified them via Facebook (as we always do) that our payment would be late and we would make a payment on September 13,2019.

- So what we get from this is that you have a history of late payments, and when you are late you tell them the date you are going to pay and figure that they have to accept it.

But it gets better...

On September 14th, I attempted to make a payment after letting Valerie know that I was at the bank getting a new debit card.

- So you are now already 1 day past the date you stated you were going to pay them.

On 09/17/19 we had a family death, we let Valerie know the issue & that we would do our best to make time to bring the payment since the online was not working

- So what happened on 9/14, 9/15, and 9/16? If you were at the bank on the 14th, you could have also gone to the dealer. Then by the 16th you are now 11 days Past Due and this should be a top priority to make the payment.

But it gets better...

Valerie said that was fine.

- So did she also say when it was "fine" to? As apparently your next attempt for payment wasn't for another 8 days.

Valerie stated that she was not at work but she would had texted her son to have him cancel the repo

- It is interesting how you seemed to have masked out the date/time of when the messages were sent.

The fact is that this wasn't an "Illegal" reposession. Even if you had made a payment, this isn't your car. You do not hold the title to the car and if the lien holder feels that you are not able to fullfill the terms of the loan they have the right to take posession of the vehicle at any time. Oh and it doesn't matter if you say you eventually pay them what you owe. That wasn't the terms of the contract..to pay them eventually. With your apparent history of late payments and this payment that was almost 3 weeks late, it seems as if they were justified.

The Dog

United StatesREAD Your Own Report!

#5Consumer Comment

Fri, September 27, 2019

You admitted being late. YOU caused a repo. End of story!